With Load Growth and Fear of Rising Utility Bills, Are Low-Income Customers Protected?

By: Justin Lindemann, Policy Analyst

With the growth of data centers, investor-owned utilities plan to construct a significant capacity of generation resources to combat the rising electricity demand. Utility customers are expected to be on the hook to subsidize millions of dollars worth of capital investments, including low-income customers who do not have the financial capacity to shield themselves from rate increases. Although many states and utilities offer low-income assistance programs, what are the states with the most considerable data center growth already doing, and are they prepared for what’s to come?

The (Data) Center of the Issue

By the decade’s end, data centers in the United States are projected to account for as much as 35 GW of demand and about 9% of the country’s electricity consumption. Though these are merely forecasts, to power the 24/7, 365-day operations, utilities plan to finance dozens of GWs worth of new generation resources from clean energy to natural gas.

According to a Goldman Sachs study, natural gas could supply 60% of the expected data center demand. This significant increase in gas is reflected in many utility integrated resource plans, including Dominion Energy in Virginia, which wants to build more than 2.9 GW of new long-term gas capacity in the next 15 years as a short-term solution to load increase. Some utilities have also resorted to proposing new payment structures in addition to planned generation resources. AEP Ohio proposed a unique tariff structure that, if approved, would require new large-capacity data centers to pay for their own transmission needs, and Duke Energy is considering contract agreements for data centers that would require them to provide upfront financial contributions to construct new generation resources to help power them.

Besides natural gas, nuclear is also seen as an option to power data centers, with various developers and data companies already examining this alternative. For example, Oklo, a California-based advanced nuclear company, has committed itself to providing its clean energy solution in response to increasing demand for AI adoption and data centers. The company announced a non-binding partnership in late May with Wyoming Hyperscale, which wants to use Oklo’s microreactor design to power a state-of-the-art data center campus using 100 MW of nuclear energy. As for data-heavy companies, Amazon Web Services bought a 960 MW Cumulus data center campus in northeast Pennsylvania in early March that will be powered by the 2.5 GW Susquehanna nuclear power plant. Nevertheless, with the construction price for compatible small modular reactors (SMRs) rising and SMRs and microreactors still far from commercialization, this reality may not come to fruition anytime soon. Plus, if new large-scale reactors are considered, the estimated $7.6 billion cost to ratepayers of the now-operational Vogtle Units 3 and 4 – which increased residential rates by about $9 a month – might dampen the prospects of nuclear as an option as well.

Either way, new resource proposals will persist as artificial intelligence and other significant data sources enter the equation as a catalyst, partly because heavy-data users like Google are experimenting with technology like AI-infused internet browsing. For context, compared to a Google search that consumes approximately 0.3 Wh per request, a single AI-powered Google search request may even consume about 23x to 30x more than, according to worst-case scenarios and research estimates published in late 2023. It is important to note that these estimations are dependent on a number of factors staying the same, including the availability of AI-based chips and the 24/7 operations of data centers at max capacity. However, as data center efficiency grows and operation procedures change, these estimates will shift.

Moreover, while the national impact of data centers is expected to take up a significant chunk of the nation’s overall electricity consumption, the most significant ramifications will be seen on a state-to-local level, especially as growth continues to concentrate in specific pockets of the country. State by state, Virginia is far ahead in the number of current data centers. The northern part of the state is considered the nation’s most significant data center market, even the world, with 35% of the globe’s hyperscale data center share – a type of data center facility that typically supports the business activities of massive data-driven companies like Google, Amazon, Meta, and Microsoft, just to name a few. The state legislature has responded by introducing bills this year to limit the provision of sales and use tax exemptions to only centers that demonstrate certain energy efficiency requirements, requiring localities to assess the grid impacts of proposed center sites, and disallowing utilities from recovering costs through their customers from electric grid infrastructure that mainly services the load coming from data centers.

Other state responses have been more mixed in their reaction, with Massachusetts – a state with about 50 data centers – introducing legislation courting new centers with a sales and use tax exemption, Michigan pushing forward with an extension of their existing data center tax exemption until mid-century, and New York – with almost 130 data centers – wanting to create an energy benchmarking program to account for high-energy infrastructure.

While the legislative and utility actions mentioned address the potential grid and energy impacts of data centers, they also touch on the future downstream cost issues associated with a utility’s response to the massive amount of incoming load growth and the capital recovery that customers, especially those that are low-income, will have to deal with.

Low-Income Load Bearers

As utilities attack the projected data center load growth issue with additional investments and emerging technological applications, the customer is positioned to help subsidize the cost through rate increases as part of these utilities’ cost recovery processes. In the case of Duke Energy in North Carolina, the utility can recoup about 10% from new construction.

However, while wealthier households have the financial cushion to protect themselves from these rate increases, low-income customers do not, so the weight of frequent or significant bill increases bears greater financial struggle. The lack of financial security for low-income households is exemplified by one’s energy burden. In the United States, the national average energy burden, or the percentage of gross household income spent on energy bills, for low-income households is 6%, according to the Department of Energy’s Low-Income Energy Affordability Data (LEAD) tool. This average is based on an estimated 51 million households that identify as low-income, which is about 42% of all households in the country.

Depending on a person’s locality and household income, the energy burden can even be higher than 30%, particularly if you live in the Southeast. Even the financial toll from trying to keep cool during the summer heat can spike a household’s energy burden, which the National Energy Assistance Directors Association (NEADA) and the Center for Energy Poverty and Climate (CEPC) reported will increase by 7.9% this year. With the expected increase in utility bills in the coming years, such a high and localized energy burden rate may become more widespread and prevalent.

Low-Income Utility Bill Assistance

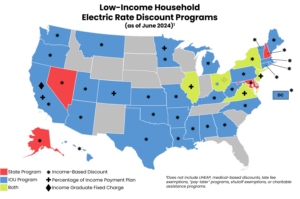

Since the reality of the energy burden in the country is not a new phenomenon, there are a number of financial assistance programs and approaches that the federal government, states, and investor-owned electric utilities have either implemented or are currently examining as options. For example, modeled after Maine’s “Project Fuel” program and created in response to the OPEC oil embargo in the early 1970s, the federal government established the Emergency Energy Conservation Program later in the decade to provide weatherization-focused assistance and eventually direct bill assistance for low-income households. It was one of the earliest programs of its kind. It would end up turning into what is now known as the Low Income Home Energy Assistance Program (LIHEAP), operating in every state, the District of Columbia, and most tribes and territories, to prevent energy-bill payment emergencies by providing payments to fuel suppliers/utilities and/or households.

LIHEAP is commonly used to determine income eligibility for several other state and utility assistance programs. However, access to the federal program has been severely limited. Federal funding for fiscal year 2024 was cut by $2 billion compared to 2023, reducing the number of low-income households served by 1 million in addition to the program’s benefits. Because of the severe budget fluctuations that each state program faces due to federal decision-making, state and utility assistance programs are critical to help fill in the gap and then some.

Many additional state and utility programs exist and vary in terms of approach and scope and can take the form of an income-based discount, a percentage of income payment plan (PIPP), and an income-graduated fixed charge, among other types of payment assistance, like late payment fee and utility shut-off exemptions. Income-based discounts entail a utility or a state providing a continuous or one-time payment attributed to an income-eligible customer, either removing the mandatory fixed charge from a bill or providing a percentage reduction of the overall monthly bill according to a specific income range, among other offers.

Then, there are PIPPs, which refer to income-specific payment plans that allow certain customers to pay only a portion of their utility bill based on a percentage of their overall income. Existing PIPPs vary in terms of their price cap. Still, no program in the country inches above 10% of a household’s income, and some programs may also determine percentage payments based on the primary heat source, electric or otherwise. This payment plan is comparable to a student loan income-driven repayment plan. It can be a helpful tool to limit a low-income household’s monthly energy expenditures and allow households to dedicate a higher share of their disposable income to pay off other bills and to put food on the table, or perhaps allow a household to establish and/or grow their savings.

There is also the income-graduated fixed charge approach, which has only recently been implemented in California. This novel method of equitable ratemaking mirrors progressive taxation, in which the lower your income, the less you must pay, and is a significant departure for investor-owned utilities in the state impacted by this change, which did not impose fixed charges before this.

The Utility Perspective on Equitable Ratemaking

To determine which approach best serves low-income communities and can garner the most support from utilities for future implementation, several state utility regulators have recently been on the case to do just that. Two such investigations began earlier this year in the competitive utility markets of Maine and Massachusetts.

The Public Utilities Commission in Maine finished its inquiry into affordable ratemaking opportunities towards the end of May this year, reporting that adopting a price cap on what utilities can charge to a low-income customer participating in an assistance program is problematic, as the compliance measures needed for such an approach could be administratively burdensome for utilities and could place them into a role of enforcement, a role the Commission did not feel would be appropriate. The Commission felt that a low-income price cap would incentivize utilities to no longer enter into contracts with low-income customers due to the hassle associated with their participation and the fluctuating income of certain customers, making eligibility determination challenging to keep up with. The Commission instead recommended that a competitive electric provider should obtain express, written authorization from customers before renewing a service contract and provide a price comparison between the provider price and the state’s standard offer.

In Massachusetts, state regulators have been investigating different low-income ratemaking options, and utilities provided their two cents on what they felt outweighed the implementation costs. Since utilities in the state are already required to provide a percentage discount to rates for certain low-income customers, National Grid, Eversource, and Unitil commented that a tiered discount rate would be the best option over PIPPs. They referenced Liberty, Eversource, and Until in New Hampshire as a model due to their existing five-tiered discount rates. Utilities supported the tiered discount approach because it allows for flexibility and lower compliance costs and removes “cliffs,” in which small income changes might result in a household losing assistance. Due to the broad income ranges and multiple tiers usually offered under a tiered discount program, the prevalence of “cliffs” would be minimized. As for PIPPs, the utilities mentioned that customers might have data privacy concerns due to the procedures required to determine one’s income eligibility. Compared to a tiered discount, the utility only needs to know the specific tier range the customer falls into. The investigation has been taking place as state regulators also examined Unitil’s proposal to increase its low-income discount rate to 40%, which was approved in late June.

Reflected by the Northeastern utilities, support for a discount-based approach is highly favored, and most investor-owned utilities in the country, albeit some with limited coverage, are already using this approach. PIPPs, on the other hand, garnered less support, which, if the utility perspective is any indication, may explain why they have only been administered in just five states and mostly through statewide regulations.

Low-Income Utility Bill Assistance in Data Center Hotspots

Circling back to the central issue, due to the influx and expansion of new data centers and the projected load to come with it, utility customers are expected to anticipate further electric rate increases, and approaches like those mentioned above would likely provide critical assistance. Examining the data center markets in the country with the largest growth and the kinds of low-income utility bill assistance that such states and their investor-owned utilities currently provide may grant an understanding of what still needs to be done to shield low-income customers in response to the projected market expansion.

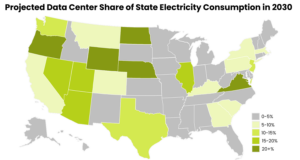

The following states are projected to have the most data center growth in the country by 2030, according to EPRI, each providing bill assistance through different approaches:

-

Virginia

-

The state enacted a PIPP via legislation in 2020, directing only Dominion Energy and Appalachian Power to collect a universal service fee. The fee funds the PIPP and its eligible participants, who must apply for eligibility through the Department of Social Services, after which the utility enrolls a customer’s account. Under Dominion, customers who utilize electric heat will have their monthly bill capped at 10% of their income. At a minimum, customers will pay $10.

-

Virginia’s projected data center electricity consumption may grow to 46% of the state’s total by 2030, compared to about 25.6% in 2023.

-

-

Texas

-

Texas offers limited financial assistance outside the state’s LIHEAP program. El Paso Electric Company, situated in the eastern tip of the state, offers a low-income discount that exempts eligible customers from paying the customer charge.

-

Texas’ projected data center electricity consumption may grow to about 10.6% of the state’s total by 2030, compared to about 4.6% in 2023.

-

-

California

-

Utilities in the state must offer various income-based discounts under either the California Alternative Rates for Energy (CARE) or Family Electric Rate Assistance (FERA) programs. Customers eligible for the CARE program may receive a 30% to 35% electric bill discount through the utility. Families whose household income exceeds those allowed under the CARE program can receive an 18% discount on their electric bill through the FERA program.

-

Pacific Gas & Electric (PG&E) also operates a PIPP pilot program until 2027 for a limited number of customers, capping the monthly electric bill at $32 for certain income-eligible customers. Those who do not qualify under the program’s income guidelines may still qualify for a $97 cap.

-

California is also the only state in the country that has implemented an income-graduated fixed charge. State regulators approved a fixed $6 charge for CARE customers and $12.08 for FERA households. The new structure also decreases the residential energy usage rate by $0.05 to $0.07 per kWh. Though the rate structure has been approved, large investor-owned utilities have been given more than a year to transition, with the latest implementation date being March 2026 for Pacific Gas & Electric – the largest utility in the state. However, around the same time the fixed charges were approved, state legislators introduced a bill to repeal the original bill that authorized the income-graduated fixed charge. The bill replaces the equitable rate structure with a $10 cap.

-

California’s projected data center electricity consumption may grow to 8.7% of the state’s total by 2030, compared to 3.7% in 2023.

-

-

Illinois

-

Illinois’ Department of Commerce and Economic Opportunity administers a PIPP for customers with an income of up to 150% of the federal poverty guideline. The payment plan caps a customer’s bill at 6% of their income, as available to a limited number of utilities, including Ameren Illinois and ComEd. The program is funded by a meter charge for other low-income assistance programs and a one-time utility contribution. The availability of program funds has been an issue, as applications have been closed since October 2023 and continue into mid-August this year.

-

Illinois’ projected data center electricity consumption may grow to about 12.6% of the state’s total by 2030, compared to about 5.5% in 2023.

-

-

Oregon

-

Oregon’s electric investor-owned utilities offer varying low-income discounts. Pacific Power uses the state median income (SMI) to establish a tiered discount structure that gives customers up to 20% of SMI a 40% discount. In comparison, those with an SMI above 20% and up to 60% receive a 20% discount on their electricity bill. Certain customers living in a multifamily residential building may receive a 30% discount.

-

Portland General Electric offers a similar discount designed to follow the SMI and established five tiers for those with an SMI of up to 60%. The highest discount a customer may receive is 60% for having an income up to 5% of the SMI.

-

Oregon’s projected data center electricity consumption may grow to about 24.1% of the state’s total by 2030, compared to about 11.4% in 2023.

-

Looking Forward

Knowing now what the fastest-rising data center markets already offer as assistance to low-income customers, it is apparent that there is a baseline of support that many customers can take advantage of. With each state offering LIHEAP payments and most utilities offering some discount to income-eligible customers, only a few provide customers with something other than a discount, going as far as capping residential rate payments altogether. Considering the significant shares of electricity consumption from data centers that each state is expected to be impacted by utilities in these states will surely propose significant capital investment reimbursements from their customers to combat the demand by the end of the decade. Millions of low-income utility customers are thus expected to be at an even greater risk of financial distress than today, and with LIHEAP facing current – and perhaps future – budgetary constraints, building out state and utility assistance has become all the more important.

In recent years, some states and utilities have implemented certain mechanisms that go beyond a simple discount, from California’s income-graduated fixed charge approach to Virginia’s PIPP program. Still, many have not equipped low-income customers with the certainty that they can withstand the weight of future bill increases, let alone the current rates. Customers may benefit from a definitive price cap or lower rates based on income, perhaps even instituting cost recovery exemptions that disallow certain customer classes from having to subsidize the cost of new resources needed to combat the energy demand from load sources that a specific class is not using or benefitting from, like data centers, among other alternatives. With the possible spike in energy burden rates across the country, building more equitable pathways to accessing rooftop or community solar may also be the key as low-income customers seek energy independence and savings. In addition, increased home energy efficiency, made possible by federal, state, and utility energy efficiency incentives explicitly designed for low-income communities, could be part of the solution as well.

All in all, as utilities plan to respond to the incoming flood of data center load by constructing additional generation resources, recovering a significant amount of capital from their customer base, one question to ask is: Will low-income customers be provided with enough protection?

Contact us to learn about our DSIRE Insight subscriptions, custom research, and consulting offerings on various clean energy technologies for interested individuals or organizations.